GATTACA!

It's about to get gross

- Messages

- 15,104

- Reaction score

- 12,943

In 1973 a $28k home was slightly above average. A $190 payment x 12 would equal $2,280 annually. 2,280/6,500 = roughly 35% of your income.We married in '73 and 10 months later had our first. Our rent at the time was $110. We got a notice that it was being raised to $135. Once we had our first one the wife quit working and our income was $6K - $6.5K. I was upset about the raise in rent and decided if we were going to pay that much we might as well own a home. We borrowed $2K from my dad for a down payment and got our first house for $28K or somewhere in that range. Our payment was $190. $135 was going to stretch us, but $190 looked impossible. Each of us owned our own cars when we married. We sold one and basically cut back or way down on everything else. Especially when #2 showed up in '75. #3 came in 81. #4 & #5 came in 85 & 86. She wanted another girl but no luck, so we quit at 5. I increased my salary to keep up by taking new jobs because they paid better. We ate a lot of potatoes back then. Bought generic brand groceries and the kids got hand me downs a lot. We didn't have two cars until around '90 when she went back to work. We improved our housing by selling after prices went up so we made enough to upgrade, but keep our payment close to the same. Once the youngest was in school, she went full time and we bought our current home. Once my salary allowed it, she quit to be home when the kids got home from school.

You can compare the COL and economy from then to today and say it's tougher now and it may be, but it's not that much of a difference as some think. It was tough back then as well. My point is if you're committed to having someone home with the kids all the time, you'll find a way.

In 2024 a average house price is around $420,000. That $2,000 downpayment loan you needed to ask your dad for is now $15,000 at 3.5%. Your $6,500 salary adjusted for inflation is $48,135, which is almost exactly what the average salary is in 2024. The payment on a $420,000 house with 3.5% down at 6.8 APR is $2,563 per month. That's $30,756 per year. Roughly 63% of your income.

It's a gigantic difference.

And before anyone starts. Yes you can find a fixer upper for less money. You can rent and try to save for years. You can sublet your house. You can add an extra revenue stream by having both spouses work. You can cut out a car and your morning coffees. Everyone is responsible for their own financial decisions. That isn't my point. My point is that the economic conditions aren't the same as they used to be. Until price gouging and corporate greed are addressed these trends are going to continue to get worse.

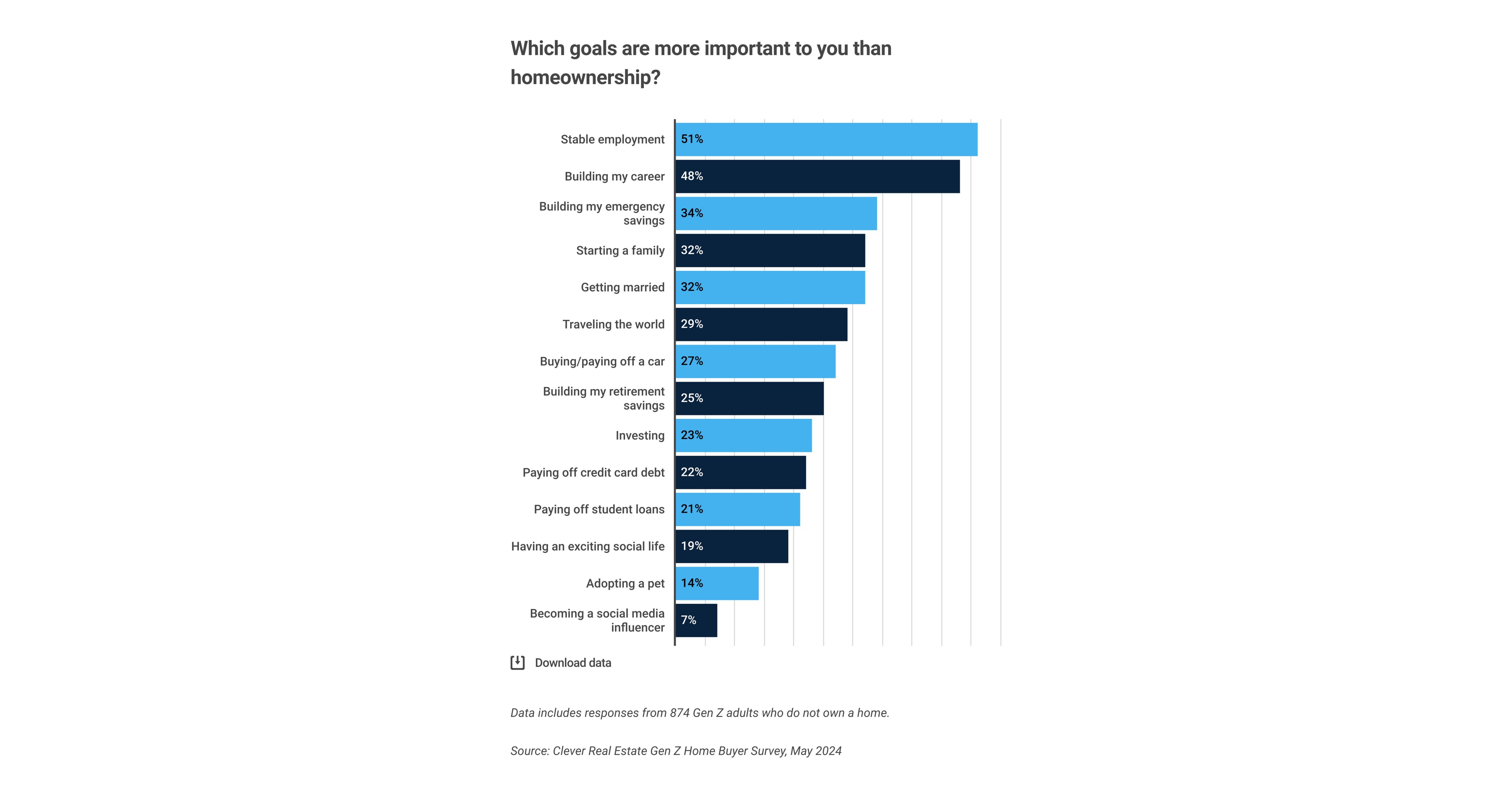

It's to the point where a majority of gen z believe they won't ever be able to own a home.

Survey Reveals 60% of Gen Z Worry They Will Never Own a Home

/PRNewswire/ -- 60% of Gen Z worry they might never own a home, with nearly all adult Gen Zers (98%) citing significant barriers to homeownership, according to...