- Messages

- 33,950

- Reaction score

- 9,294

And here's an essay by Marco Rubio titled Common Good Capitalism and the Dignity of Work in Public Discourse:

That was absolutely fantastic. A quintillion reps to you Whiskey.

And here's an essay by Marco Rubio titled Common Good Capitalism and the Dignity of Work in Public Discourse:

America is getting older. Indebtedness is rising. Economic recoveries keep taking longer. This is not a coincidence.

[Click through for graph]

We’re now in the longest economic expansion in US history, so it’s as good a time as any to think about how the next recession will play out.

In theory, recessions should be getting some combination of rarer and milder over time. We have better data (thanks to the work of an army of technocrats starting in the 30s), and we have better theories (every recession refutes at least one theory of recession-prevention). It’s possible to imagine shifting to a regime where economic growth is oscillates in a tighter range, and never goes below zero.

This, of course, doesn’t happen. There are partisan theories as to why — the Evil Republicans theory of unrestrained speculative excess, the Evil Democrats theory of excessive regulatory meddling — but the more interesting ones are politically-agnostic. I’m partial to Hyman Minsky’s argument that the process goes like this: in good times, few loans default, and credit spreads narrow; investors’ return expectations are sticky, so they respond to lower spreads by levering up; at some point, what would be a minor speedbump at low leverage turns into a crisis with higher leverage, leading to a funding crisis and a deflationary unwinding.

What’s convenient about this theory is that it embodies enough human wisdom to explain that we’ll never fully solve the recession problem. As another expert on the human condition might have put it, the poorly-calibrated risk models you will always have with you.

But Minsky runs into the same problem as every other economic theory: if it’s universal, it’s also smug. Minsky doesn’t tell you what will go wrong; he doesn’t say “That’s why you’ll have a maturity mismatch between commercial paper funding and illiquid structured credit in 2008,” just that something, some day, will go wrong. That’s frustrating, because it’s not action-guiding, and the whole point of understanding recessions is knowing when to short equities in size.

Predicting recessions while policymakers are trying to prevent them is a metagame: you’re trying to figure out what the Fed, Congress, and the President either can’t or won’t stop. That’s a two-step problem. You need to enumerate forces that governments can’t control, and you need to figure out which tools will become surprisingly ineffective.

The Irresistible Force of Demographics

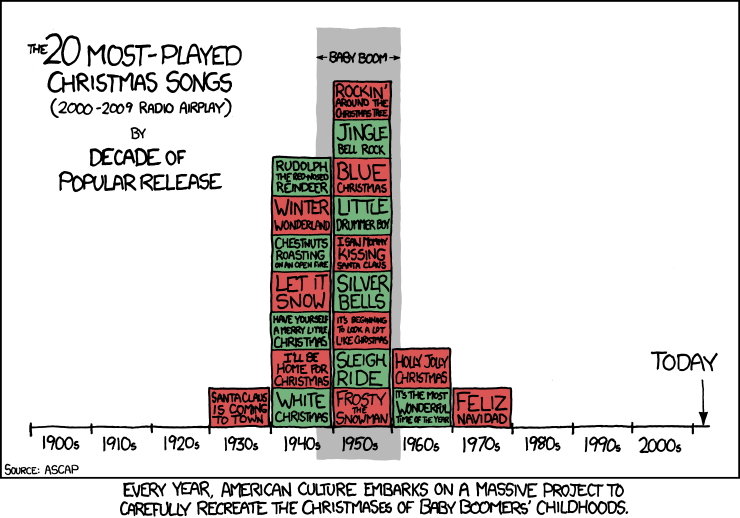

There’s one phenomenon too big for any American political party to stop. The Boomers. They’re an immense generation, and they’ve been distorting the economy for decades. From 1950 to 1970, college enrollment rose from 2.2m to 6.7m. In the 70s, we had high inflation — oil was a factor, but a bigger factor was the biggest generation in history buying homes, cars, and appliances. In the 80s, the boomers already owned houses, and they started buying stocks. In the 90s, more stocks. In the 2000s — panic! They’d overinvested in equities to compensate for undersaving, so they switched to an investment category that offered more leverage: housing. We know how that turned out.

And now, they’re retiring. Retirees do two things with assets: they sell them down, and they rotate from risky products like equities and mortgaged-to-the-hilt houses to safer stuff like T-bills and annuities.

[Click through for graph]

The boomers are an important phenomenon, and no generation has so assiduously tried to understand itself. It’s always best to get an outsider’s perspective, so I picked up a copy of the definitive opus on the generation.

[Click through for graph]

Harsh!

Gibney’s book is informative, and quite entertaining. If you want to argue with him, I recommend reading it. If you read the title and decided to hate him, I’ll help you out there: check out this interview he did with his tailor, featuring a photo where he poses with a Juul.

Generation of Sociopaths is thorough and well-researched. But it’s part of a longer literary tradition in which mild misanthropy gets applied to particular anthropes. A few other titles that might work just as well:

Seriously, he does not like the Boomers. But there’s always the question of whether they’re special because they’re bad, or special because they’re numerous. Any demographic bulge causes problems — there’s a lot more civil unrest in South Sudan (average age: 17) than in Japan (average age: 47). Meanwhile, Japan suffers from a capital surplus and slow economic growth. As the boomers shifted the US’s average age lower, we faced young-country problems like unrest and inflation; now that the boomers are making America older, we have old-country problems.

- Protocols of the Elders of Woodstock

- The Eternal Boomer

- The Rising Tide Of Boomerdom Against Below-Retirement-Age World Supremacy

- The Camp Of Saints (Who Were Born Between 1945 and 1964)

Many of the trends we’re dealing with today — financialization, globalization, inequality, cultural stasis — can be chalked up to a combination of two factors: first, things the Baby Boomers have in common with anybody else who grows up in a time of comfort and abundance; and second, the impact of sheer numbers.

🎵 🎵You will get a gloomy sinking feeling when you see 🎵 🎵Retirees per worker soar and wreck the whole economy 🎵 🎵

In my capsule summary of the late twentieth century above, every decade was defined by the Boomers’ demographic bulge; we’re still a few decades away from that bulge ending, but if Boomers are the swing factor, the 2020s and 2030s will be defined by: rising healthcare expense, selling pressure on equities and residential real estate, demand for treasury bonds and other safe assets, and a political bidding war for the elderly vote. The political dimension is especially important, because while Boomers will not be the largest generational cohort much longer, they’ll be the largest voting cohort for a while yet. Presidential election turnout was 70% for people over 60, compared to 46% for people under 30. And in off-elections, it’s more extreme: 65% versus 36%.

So in 2020, Baby Boomers will be around 21% of the population, they’ll represent around 39% of the votes cast. They will probably vote more or less like everyone else: they’ll vote for their own interests within an Overton Window defined by their principles. Voters in most countries are uncomfortable with pure giveaways; nobody is going to run on a platform of “raise taxes in states that voted for my opponent, use those to fund Basic Income for my supporters.” But within the range of acceptable outcomes, people like to vote for what they want to get. This is dangerous, because in the US the Overton Window doesn’t set many limits on how much we can tax workers and investors to transfer wealth to retirees.

Big Generations and the Savings Problem

Whenever a country suddenly has a lot of young people, the clock starts ticking: they’re about sixty years away from having a lot of old people. Broadly speaking, there are two solutions to this problem:

- Grow the population, so the pyramid remains balanced.

- Defer more consumption than usual so you have assets to live off of when you’re older.

Unfortunately, the US has collectively chosen option three, which is to do neither of these things and then see what happens.

To be fair, it’s a new problem. For most of human history, life expectancy was under 40, mostly driven by high infant mortality. There’s an annoying paucity of data, leading to all sorts of contradictory claims here — hunter-gatherers got lots of exercise and had great diets, so maybe they all died old[1]. On the other hand, modern hunter-gatherers have ridiculously high homicide rates, so it might be a moot point.

We do start to get good data in a few countries in the last 200 years. In England and Wales, 50-year-olds had a life expectancy of around 70 from 1850 to 1900, which steadily rose to 75 by 1950, and is now in the mid-80s. Or, to put it in starker terms, if you expected to stop working at 65, your years-in-retirement have risen from 5 to 17 in the past century. These work as a proxy for life expectancy trends in countries that have access to modern medical technology and are mostly unconstrained by costs.

[Click through for graph]

Given the rise in rich-world life expectancies over time — which has only slowed in the last few years — you’d expect a meaningful rise in savings rates over the same period. That’s not what we see, though: US savings rates peaked around 1975, dropped steadily until the mid-2000s, and recovered slightly following the Great Recession:

[Click through for graph]

Savings rates trended down as boomers became a larger proportion of earners, but young people generally save less, and their savings rates trended down further in the 2000s, only turning around post-recession:

[Click through for graph]

The worrisome possibility is not that the boomers are uniquely bad, but that they’re not especially bad but very numerous.

“Savings” can somewhat obfuscate what’s going on, though. Someone burying coffee cans full of cash in the backyard is saving, but so is someone who buys equities.

We can break the options down like this. If your expected future expenses rise, you can either:

- Save more and consume less, or

- Save the same amount but take higher risk — and you can do that by either A) Taking discrete, tangible risks; switching careers, starting a company, making yourself an expert in a field that you think will pay well in a decade, or B) By looking at a menu of investing decisions with consistent risk/reward payoffs, and choosing the one with the highest risk and reward, perhaps levering up to do so.

Baby Boomers took advantage of both options. Microsoft and Apple, for example, were both founded by Boomers, and both had distinctive and unconventional visions. But it’s hard to take unusual risks like this, especially if you’re thinking about risks only when you start calculating how much money you need for retirement (Gates founded Microsoft at 19; Jobs founded Apple at 20).

So the default approach is to take the usual risk, only more so: in the 90s, people worried about their retirements rotated their stock portfolios from stodgy companies to tech. That didn’t work; tech outperformed from the mid-90s to the end of the decade, then collapsed. Since investors form their expectations by looking backwards, expected returns for stocks declined. The UBS/Gallup survey showed that in 2000, equity investors expected one-year returns of about 16%. By 2002, expected returns were 6%. In the 2000s, the move was to lever up by buying bigger houses with lower down payments.

The two broad approaches to risk — differentiation and leverage — have distinct macro effects. Starting a new company creates exogenous upside uncertainty: the world will be different if it works, probably for the better, but it’s hard to say exactly how. Levering up, on the other hand, doesn’t directly change the state of the world, it just changes who collects which tranche of returns. If you buy the house you can afford with a 25% down payment, a 10% appreciation in its value makes your investment worth 40% more. If the same sum of money is a 5% down payment, a 10% increase in your home’s price means a 200% gain. But the larger mortgage means that a larger dollar amount of the home price appreciation accrues to your lender, not to you — they earn the first (1 — down payment %) * (interest rate) of returns, every single year. You’re buying a higher-strike option on the same basic asset.[2]

Leverage doesn’t just shift the same returns around, though: it also creates externalities. Specifically, access to capital allows businesses to grow faster than they otherwise would, which creates wealth. However, higher leverage in general raises the odds of financial crises, which destroy wealth. As a rough rule of thumb, for leverage to create wealth on net it’s necessary but not sufficient for it to involve production, not consumption. So giving consumers more leverage to buy bigger houses just adds to the risk of a crisis without making the world better off.

It’s instructive at this point to compare the US to other countries that dealt with baby booms, especially the East Asian “miracle” economies. For much, much more, see my writeup here, but for now what’s worth pointing out is that a) Japan, Korea, Taiwan, etc. did fuel their growth with leverage, but b) this leverage was heavily weighted towards manufacturers, not consumers. Consumers faced high implicit and explicit tariffs on consumer goods, and artificially low interest rates on savings, which allowed banks to lend money to growing companies at scandalously low yields.

The result of this is that Japan and its neighbors have a huge capital base, and hard-to-assail positions in capital- and knowledge-intensive goods. That’s a way to induce positive-sum savings, at least at the country level: your future income comes not from selling appreciated assets, but from selling Toyotas, ships, and semiconductors to the rest of the world.

In the US, we didn’t exactly do this. We certainly found things to sell to the rest of the world, but many of them were claims on our future income.

Housing Bubbles, Just-in-Time Inventory, and the Great Working Capital Shift

There are two parallel trends over the last four decades that have changed how fiscal and monetary policy work without changing what they do. First, Americans own bigger houses with bigger mortgages. Second, American companies have become allergic to holding any more inventory than they need.

These trends happened for fairly unrelated reasons, but the combination led to some interesting side effects.

Historically, the way recessions worked was that companies accumulated excess inventory, so they laid off employees to work off the overhang. When one company does this, it’s fine, but when enough companies do it at once, they reduce aggregate demand, which makes the inventory overhang bigger, leading to more layoffs. That’s a simple model that ignores financial markets, but when financial markets are small, or the main source of funds is the banking system rather than capital markets, it’s pretty accurate.

In that model, governments can stimulate growth by a) raising spending, to stimulate demand, b) cutting taxes, to encourage investment, and c) cutting interest rates, to reduce the cost of carrying excess assets on the balance sheet.

When companies are allergic to holding inventory, though, it becomes a weaker channel for stimulating growth. This clearly took policymakers by surprise; back in the 90s, Alan Greenspan once told a metals trade association “Every day, I still look for the price of №1 heavy melt steel scrap.” In his career as an economic consultant, scrap steel prices were a great early indicator of economic health, but by the end of his Fed tenure, China was producing four times as much steel as the US, and container shipping had tightly linked their economy with ours. Shipping costs are a bigger share of scrap metal’s price than they are for finished goods, so the market is somewhat localized, so it’s hypersensitive to local rather than global conditions.

All this sets up a situation in which central banks’ models are tuned to an economy that no longer functions the way they expect it to, which means they get the wrong signals. In a manufacturing-heavy economy, interest rate cuts quickly flow through to manufacturing employment by way of inventory.

Actual changes in inventory still show a lag, because a reduction in demand coupled with continued production increases both how much inventory a company has and how long it takes to sell it (e.g. if you assume that demand is $1m/month and have three months of inventory, and then demand drops to $800k/month but it takes you three months to react, your inventory has risen to $3.6m, or 20%, but your inventory-months have risen from 3 to (3.6/0.8 = 4.5, or 50%)

This is easiest to see with a long-term chart: from the 50s through the mid-60s, inventory’s contribution to GDP volatility was in-line with its contribution to GDP. As inflation picked up in the late 60s and through the 70s, inventory contributed more to GDP volatility than to GDP growth (i.e. manufacturers tended to overreact to inventory changes — a Fed that’s constrained by inflation risks can’t seamlessly react to drops in demand). Starting in the 80s, inventory volatility and inventory contribution to GDP growth became deeply decoupled, as companies shifted inventory risk off their balance sheets and on to those of consumers and offshore suppliers. And in the 2000s, we reached the natural endpoint of this trend: inventory’s contribution to GDP growth turned somewhat negative — GDP growth was slightly positive from the 2006 peak through 2011, but real inventories had a net decline over this period.

[Click through for graph]

Also included in the chart is the steady decline in total inventory as a percentage of total GDP, from around a quarter at the start to roughly 15% today.

Dangerously for economic policymakers, monetary policy continued to work, just through a different channel: instead of encouraging companies to produce more, it increasingly encouraged consumers to spend more. In the aggregate, this is not necessarily a problem; whether production leads to wage growth and spending growth, or spending growth leads to production and wage growth, the net effect is the same.

The problem is the side effects: lower rates increase the value of real assets, and increase the consumer’s ability to turn asset appreciation into spending. This can happen through liquidating assets, or, in the case of mortgages, through taking advantage of the cheap option to refinance them.

And the side effect of this ties back to demographics. If you bought a big house to raise a family, and your kids have moved out, your surplus residential real estate is basically a speculative asset. You own more housing than you need, but when home prices rise that just makes you financially better-off. A house that’s bigger than you need is not just an investment, though; it’s a warehouse. To someone who owns more real estate than they need, housing price appreciation a) gives them more money to spend, and b) means they have somewhere to put all the stuff they want to buy.

The reductio ad absurdum of this is using a home equity loan, or a mortgage refinancing cash-out, to fuel spending. Total mortgage cash-outs were over 1% of GDP from 2001 through 2007, and over 2% at the peak of the housing bubble in 2005–6. Growth in home equity cash-outs was around 8% of GDP growth during the bubble, and a drop in home equity cash-outs accounted for over 100% of 2008’s Y/Y decline in GDP. Earlier in the bubble, we can see cash-outs as a lever for improving GDP growth — in 2001, as the tech bubble rapidly popped and the Fed cut rates from 6% in January to under 2% by year-end, home equity cash-out growth accounted for $75bn of the economy’s $220bn GDP increase.

[Click through for graph]

But to the younger generation, housing is not just a retirement plan with an early-cashout option. It’s mostly an expense — and, crucially, it’s the expense that determines when they will have kids.

The aggregates only tell an accurate story when you fail to account for demographics. Once you know demographics are a factor, monetary stimulus imposes negative externalities: it makes older asset-owners better-off at the cost of preventing younger people from accumulating assets. As inventories have declined and total consumer debt has risen, monetary stimulus has subtly flipped from being pro- to anti-family formation.

You can imagine a fix for this: give the Fed a triple mandate. Instead of stable prices and high employment, require them to aim for stable prices, high employment, and stable fertility rates. And if you really want to get clever, consider this: price stability matters less when population growth and GDP per capita growth are high, because you can devalue older savers’ assets today and compensate with higher absolute transfer payments backed by your larger economy in the future. This is not just theoretical: Japan and Korea both tolerated high inflation early in their growth cycles, because it paid for the infrastructure that gave them a better safety net later on.

Unfortunately for central banks, it’s hard to raise household formation rates through monetary policy alone. One option might be for Congress to set an annual maximum EITC or Basic Income, but to let the Fed choose the actual level. This way, the Fed could combine monetary tightening with a higher EITC to redistribute money to wage earners, or raise and lower both in tandem to achieve traditional policy goals.

There is roughly zero chance that it was intentional, but economic policy in the Trump administration has, ironically, improved this situation relative to Obama, Bush, and Clinton: by ramping up deficit spending in a strong economy, Trump a) makes a tighter monetary policy relatively more feasible, and b) redistributes some of the benefits of economic growth from owners to earners. It isn’t what a utilitarian technocrat would have wanted, since it’s so skewed to the biggest earners who are already pretty big asset owners, but giving a tax cut to almost two thirds of households does have an impact on the economy, even if most people don’t realize they got it.[3]

The Implicit and Explicit Balance Sheet of Retirees

My broad thesis is that a shift in how monetary policy stimulates the US economy has led to wealth redistribution to older people, whose high propensity to vote means their interests are entrenched. But this doesn’t address the narrower question of what investment decisions they’ll make, and under what constraints. Specifically, we should ask what effect growth in the retiree population has on economic growth and price levels.

Obviously, retirees slow economic growth, because they don’t work. In a closed economy, retirees would also be inflationary, because while they stop earning, they keep spending, at roughly ⅔ of their previous rate. But in a more open economy with levered balance sheets, mass retirement can be deflationary instead, as they delever and sell risk assets to buy safer stuff. If you’re 55 and thinking about retirement, you might be tempted to map out the options this way: “If I take lots of financial risk right now, I can quit working in five years if those risks pay off; if they don’t, I’ll have to work a bit longer, but I can still retire at 65 with the same standard of living.”

As you get older, though, either a) this happens, or b) you realize it won’t. So, either you quit working, shift your portfolio from stocks to bonds, and move to a smaller house, or you make those shifts, sell those assets, and cut your expenses sooner.

This means that an economy weighted towards services has a natural level of cruise control: people don’t have to stop working, but they can slow down. A manual laborer has to save a lot, because one back injury can mean retiring at 45 instead of 65, but office workers don’t have this concern. However, this countercyclical tendency has a major drawback: the output of service jobs harder to measure, so employers weight experience more.

We know these jobs have hard-to-measure outputs both intuitively (it’s easier to see where the assembly line is backed up than to figure out who in HR or accounting messed up) and through appeals to authority: Alan Greenspan is one of history’s great economic-data nerds, and his single most famous speech includes an extended riff on how hard it is to measure the value of things like software, legal opinions, and medical operations.

Greenspan ultimately concluded that we’d probably underestimated productivity growth in the services sector, but this was a sort of arbitrary decision. It also was a way to justify not raising rates in the late 90s, which was followed by a collapse in equity prices, so maybe we shouldn’t take it too seriously.

Greenspan is not the only economist to muse about how hard it is to measure service sector productivity. William Baumol had some thoughts there, too. Specifically, Baumol noted that the productivity of members of a string quartet hasn’t risen at all since the nineteenth century; they still produce the same number of minutes of live performance per minute of work. And yet, we can’t pay them nineteenth-century wages, or they’ll get 2,000% raises by working in fast food. Per Baumol, as productivity in manufacturing and agriculture rise, more people end up working in services, but any service job involving one-to-one in-person interaction has no meaningful way to increase productivity. So, over time, economies suffer a sort of heat-death, where the sectors that can grow output per hour become a smaller and smaller fraction of hours worked, until the main constraint is the cost of finite raw materials.

Service-based economies tend to have milder swings. Even the heat-death thesis assumes a slow glide path to stasis. We see this in the data already. The Great Recession, the most severe postwar economic contraction, led to a 5% drop in GDP. The mildest recession in the period from 1880–1945, the period for which we have good comparable data, involved a decline over 8%.

Meanwhile, let’s consider the balance sheets of our services-heavy economy. The Fed offers a triennial Survey of Consumer Finances, and the New York Fed offers quarterly data on consumer credit. Between these two, we can get some rough estimates.

First, the old are rich: in 2016, median net worth for households 65–74 was $224k, versus $97k for the country as a whole. That makes sense, of course. Your net worth should bottom out when you’re first forming a household, and should peak when you retire and slowly drift down from there. But it doesn’t: over-75s have a median net worth of $265k. Ten years after the standard retirement age, the average family is richer. This has not always been so, and the numbers are volatile, but in general the net worths of the very old are trending up.

What explains this? Looking at the 1989 vs 2016 breakdown by age and asset type, older families’ median ownership of retirement accounts rose $48k, as the number of older families with retirement accounts rose from 6% to 41%. However, this wasn’t just because people shifted savings into tax-advantaged accounts; older families’ median ownership of stocks rose $9k ($5k in 1989 to $14k in 2016), and their mutual fund holdings also rose (from just over $3k to just over $24k). Younger families’ net worths in these categories have risen, but not by nearly as much. It’s a truism, whether you read the biographies of successful investors or look at the Fed’s data on net worths by age: the most prudent financial strategy is to do as much of your asset accumulation as you can in the early 80s, when everything is screamingly cheap.

Home ownership tells a similar story. The cadence of home ownership over one’s lifetime has shifted in the last three decades:

[Click through for graph]

In general, older people are holding on to their homes a bit longer, and younger people are a bit less likely to own.

If we break these numbers down by median home equity by age, the reason becomes apparent:

[Click through for graph]

It’s gotten expensive to own a home! Those younger savers will still mostly buy homes — eventually. But it will take them a few more years, which means they’ll delay having kids by a few years, which means, thirty or forty years hence, fewer workers per retiree.

On the liability side, there’s another factor besides high home prices: high student loan debt. Among adults over 40, mortgage debt is typically about 70% of total debt, but of the $970bn in debt owed by 18- to 29-year-olds, 38% is student debt.

One way to look at this is to argue that older people are enjoying a pretty healthy economy, as their jobs and their assets are both well-defended by the government’s policy decisions. But this prosperity comes at the expense of young people, who are in a sort of balance-sheet recession; they can’t afford to invest until they’ve paid down their debts, so they delay home-buying and family formation.

(Perhaps the only upside here is that student debt, unlike mortgage debt, doesn’t force you to stay in one place if you’re financially underwater. The sunk-cost fallacy, however, does encourage you to stay in one career. The only thing more demoralizing than owing $50k in student debt for your masters in photography is owing that much money and not being a professional photographer.)

Explicit balance sheets are only part of the story. There’s also the implicit balance sheet: the liabilities that constitute expected future spending.

As people age, they travel less and spend less on food — calorie needs decline by 10–15% from middle age to old age, and senses of taste and smell weaken, too. This means that the elderly are less exposed to fluctuations in food and fuel prices, the two CPI components that get excluded from the core metric because they’re so volatile. People over 65 have access to Medicare, have social security benefits indexed to costs of living, have a 79% home ownership rate (compared to 65% for the US as a whole). They don’t have to spend money on education, either.

In short, the non-financial asset portfolios of the average retiree make them the most inflation-protected group around. Old-person CPI growth is well below the national average. This has an important implication for their financial portfolios: it means that they get a better real return on treasuries than other investors would.

For the Boomers, the twentieth century was awesome, but the twenty-first has left a lot to be desired. First, the equity bubble popped, so they had to find a new way to save. They chose housing, then that popped, too. They’re still well-off, with portfolios weighted towards both homes and equities. The only alternative is fixed-income, and with the ten-year yielding 1.78%, that’s not too attractive.

But a high home-ownership rate among the old means that as people either move to retirement communities or die, they need to liquidate housing. And a drop in the labor force, coupled with continued anemic growth in productivity, puts pressure on GDP growth, which compresses equity valuations. Retirees have a long time to live, and if their assets start to depreciate they may shift to thinking of capital preservation over capital appreciation. And that’s when their effectively lower inflation rate kicks in. The richest demographic in the US — the richest group in human history, as a matter of fact — has just one asset class to rebalance into.

[1] Hunter-gatherer skeletons imply that not a lot of them lived past sixty, but paleo diet people have correctly pointed out that if you avoid grain and sugar and do lots of high-intensity exercise, your bone density will be that of a younger person. Maybe those young-looking skeletons were actually the skeletons of Art De Vany-looking old guys.

[2] Obviously a $250,000 house and a million-dollar house are not identical, but in both cases they’re proxies for the same long-term variable: local wages. In the pre-crisis period, housing prices were also tightly correlated to one another because most housing purchases were funded by sales of other homes, so a drop in one home’s price meant less funding for the next. Now that institutional investors and iBuyers are involved, the correlation is weaker.

[3] Can you really write about the impact of boomers on politics and economics without spending a bunch of time on Donald Trump?

Superficially, Trump is exhibit A in any boomer-hater’s compendium of complaints. He got a cheap college education, didn’t go to Vietnam, got rich by levering up real estate, has had multiple messy divorces, and gets a lot of his political insights from cable TV. But he is in many ways an outsider to the boomer experience. He didn’t go to Vietnam, but he didn’t go to Woodstock, either. His career trajectory hasn’t been a smooth upward climb, wafted ever-higher by a favorable labor market and soaring asset values. No, Trump has had a massively negative net worth, and has been widely seen as finished in all three of his careers. His political career was viewed as over as recently as November 7, 2016.

While he’s chronologically a boomer, and somewhat fits the narrative, he’s also very much an outsider. He missed all the fun stuff. This even shows up in his personal life: Trump was famous for showing up at all the flashiest clubs, but doesn’t drink or do drugs. He could, and did, get into Studio 54. But — we have to ask, and he surely asked himself — what was Donald Trump actually doing there?

Certainly, Trump represents something about the boomers. He represents something to them, too: he handily lost the younger vote, and handily won the older vote. In one sense, he represents that generation’s view that everything is fine as long as they’re in charge, and ideally being ruled by a paragon of their virtues. But his whole campaign was premised on the idea that, after decades in which the baby boomers were the country’s most important electoral force, things are not fine.

Trump is, like many fascinating literary characters, both an insider and an outsider. The culmination of boomer dominance and the rejection of what that dominance has entailed.

So, uh, let’s forget about Trump — it would be nutty to ignore that particular elephant in the room, but pointless to over-litigate his impact.

- Nearly 100 companies in the Fortune 500 had an effective federal tax rate of 0% or less in 2018, according to a new report.

- The report looks at the first year since the Tax Cuts and Jobs Act of 2017 went into effect.

- The list of companies covers a wide range of industries and includes some of the biggest companies in the United States.

Nearly 100 Fortune 500 companies effectively paid no federal taxes in 2018, according to a new report.

The study by the Institute on Taxation and Economic Policy, a left-leaning think tank, covers the first year following passage of the Tax Cuts and Jobs Act championed by President Donald Trump, which was signed into law in December 2017.

The report covers 379 companies from the Fortune list that were profitable in 2018 and finds that 91 paid an effective federal tax rate of 0% or less. Those companies come from a wide range of industries and include the likes of Amazon, Starbucks and Chevron.

The new tax law lowered the statutory corporate tax rate to 21%, but the companies in the report paid an average rate of 11.3%. Fifty-seven companies paid effective rates above 21%. The report was first covered by The Washington Post.

The lower average rate means that the federal government brought in about $74 billion less in corporate taxes than if all the companies had paid the statutory rate, according to the report. (cont)

By many measures, the U.S. economy is doing well. Unemployment is near a 50-year low, consumer spending is strong and the stock market is delivering solid returns for investors. Despite these positive indicators, public assessments of the economy are mixed, and they differ significantly by income, according to a new Pew Research Center survey.

Majorities of upper-income and middle-income Americans say current economic conditions are excellent or good. But only about four-in-ten lower-income adults share that view, while a majority say the economy is only fair or poor.

(cont)

In a reply to Owen White’s comment on my last post I claimed that English Toryism worthy of the name suffered its final defeat in 1846 with the triumph of the free trade movement and the abolition of the Corn Laws. To explain what I meant I want to consider the account of the anti-conservative nature of capitalism in The Communist Manifesto. Marx and Engels point out that bourgeois capitalism has dissolved the feudal ties that used to tie men to their ‘natural superiors,’ and that it has stripped human relations down to ‘egotistical calculation,’ and reduced human values to ‘exchange value.’ But they think that this was in a way necessary (one might almost say good) because it has enabled the rise of a revolutionary class who know that they are being oppressed: «for exploitation, veiled by religious and political illusions, it has substituted naked, shameless, direct, brutal exploitation.» (p. 16) But what if the religious and political institutions that founded pre-capitalist society in Western Europe were not illusions? What would become of their argument then? If one thinks that earthly societies ought to reflect the hierarchical order of the cosmos, then one might indeed think that ‘feudal’ society may have been more defensible then Marx and Engels thought, and that the rise of bourgeois capitalism was not a necessary unveiling of exploitation at all, but just an unmitigated disaster.

It is worth recalling some of the basic points that Marx makes about capitalism and its exploitative character in order to contrast it with pre-capitalist society. (The following paragraphs are taken from a longer writing project of mine, and involve a bit of ‘technical detail’).

The most fundamental insight of Marxian economics is the distinction between use value and exchange value, and the most basic Marxian critique of capitalism is that it subordinates the former to the later. But in so-called ‘feudal society’ such a subordination had not taken place. The Aristotelian-Marxist Scott Meikle makes a similar point with respect to ancient ‘economy’:

In order to capture the difference between capitalist economy and pre-capitalist ‘economy’ the distinction required is that between use-value and exchange-value. The most fundamental question to be asked about a society is which of these predominates in it. A capitalist society is predominantly a system or exchange-value; economics is the study of the developed forms of exchange-value and of the regularities in its movement, or ‘actual market mechanisms,’ and it can come into being only with the appearance of full-blown market economy, that is, with markets in labour and capital, Antiquity was predominantly a system of use-value, partially administered, and if it had regularities, these were nothing like the cycles, laws, and trends which characterize a system of exchange-value. (p. 167)

Meikle is talking about ancient Greek society, but a similar point could be made about feudal society.

As Meikle shows, Marx’s theory of value is largely a development of the account of exchange offered by Aristotle. Marx himself notes that Aristotle was the first thinker to distinguish between use value and exchange value. Although Aristotle did not use a word equivalent to “value,” he recognized that external (i.e. material) things possessed by human beings could be used in two different ways. The first and original way that they could be used, the reason why people first begin to take or to make things in the first place, was to fulfill some human need (chreia).

Now, while neither Aristotle nor Marx developed this point much, I think it is important to point out that the relevant kind of need here is what Aristotle calls “hypothetical necessity”: if persons are to live they require food and shelter, if they are to live well they will need certain kinds of things of a certain quality. What things in particular they need depends on the hypothesis— that is, on their conception of the good life. If, for example, the good life is seen as requiring conviviality they will require wine, pleasant tasting food, musical instruments and other things useful for celebrating feasts. If it is conceived of as requiring the contemplation of beauty the will need statues, pictures, beautiful buildings, and so on. Marx glosses over this point, giving his conception of use value a somewhat “naturalistic” tinge, as though human needs could be simply given. This is a point on which radical Orthodox theologians such as John Milbank and John Hughes have criticized Marx. They have argued that Marx’s theory of value should be complemented by that of John Ruskin, who argued that value depends not only on the intrinsic usefulness of things for life, but also on the virtue (or “valour”) the persons using them. Only if persons have a good conception of the good life (this conception is of course heavily influenced by culture), and the virtues necessary to pursue it, can things have true value for them.

Things thus have a value that comes from their ability to satisfy needs, and this is what Marx (following classical political economists) calls ‘use value.’

The second use of things that Aristotle distinguishes is their use in exchange. Aristotle uses the example of a shoe to explain this:

A shoe is used for wear, and is used for exchange; both are uses of the shoe. He who gives a shoe in exchange for money or food to him who wants one, does indeed use the shoe as a shoe, but this is not its proper use, for a shoe is not made to be an object of barter. (Politics I.9 1257a6-13)

Things thus have a value that comes from their ability to be exchanged, and this is what Marx calls ‘exchange value.’

For an exchange to be just the things exchanged must be of equal value. But this raises a problem, because exchange comes about between people with different needs and with different things to exchange: «it is not two doctors that associate for exchange, but a doctor and a farmer, or in general people who are different and unequal.» (Nicomachean Ethics, V.5 1133a16-18) How can things as different as a farmer’s crops and a physician’s medicine and treatment be equal? What is the common measure between them in virtue of which they can be said to be equal? As Meikle puts it:

The essence of Aristotle’s problem is to explain the capacity products have to exchange in non-arbitrary proportions; to discover the dimension in which products that are incommensurable by nature can become commensurable…

Aristotle tries different hypotheses for explaining exchange value. First money, but this will not do since one would still have to explain what makes money commensurable with other things, and then need, but need is an accident of the persons exchanging, not of the things, and does not therefore explain the ability of the things to be equated in an arbitrary way. Aristotle therefore concludes that there is no scientifically satisfactory explanation for the commensurability of such widely different things, but that must be assumed to be commensurable for practical reasons.

The classical political economists Adam Smith and David Ricardo thought that there was indeed a common measure underlying the exchange value of all different products—namely, the labor (Smith), or, more precisely, labor time (Ricardo) needed for their production. Marx, however, showed that this is only really true in a fully capitalist economy, which Smith and Ricardo falsely naturalized and universalized. Marx shows that it is only in a capitalist economy that “socially necessary labor time” (note the important addition) is converted into value. What is socially necessary is determined by competition and can be changed by innovation, but the necessity is stable enough to enable commodities to be exchanged in non-arbitrary proportions.

Aristotle argues that exchange arose naturally from the fact that some have too little and others too much of certain needed goods, and that first form of exchange was simply one good for another. Marx represents this form C–C (C stands for ‘commodity’). Then money is interposed to make exchange easier, yielding the form C–M–C [(commodity)–(money)–(commodity)]. Historically, this view is almost certainly false, as David Graeber as shown, early economies depended on distribution rather than exchange, and that systems of impersonal exchange arose after the invention of money. Nevertheless, Marx and Aristotle are right about the way money functions in an already developed exchange market. Aristotle saw the form C–M–C as natural, and as being part of the art of managing a family or a city. Since the family or the city need certain external things to live, and to live well, there is a natural art of wealth getting, which is concerned with satisfying those needs—that is, in Marxist terms, with the acquisition of use values.

But, Aristotle goes on to argue, there is a second kind of wealth-getting that is not natural, because it is not ordered to acquiring necessary instruments (use values), but rather to getting as much money (i.e. as much exchange value) as possible. This second form of wealth-getting is most clearly seen in retail trade, in which someone takes money to the market rather than goods, buys goods with the money, and then exchanges them for more money. Marx would represent this form M–C–M´. This form of wealth-getting has no natural limit, since it is not ordered to getting certain needed goods, but just to increasing the quantity of money (that is, of the exchange value measured by money). Thus, there is no reason why M´ should not be again invested to yield M´´.

On Meikle’s reading, Aristotle thinks that this kind of wealth-getting can take over and corrupt almost any kind of human activity:

Aristotle’s deeper criticism [..] is not primarily of kapelike [trade] at all, but of its aim, the getting of wealth as exchange-value, and this is a more general thing (1257b40–1258a 14). People may pursue that aim by means of kapelike […] but they may pursue it by other means too, Aristotle instances the military and the medical arts, but he means that almost anything people do, and every faculty they have, can be put to the pursuit of exchange-value (1258a8—10). All these human activities, medicine, philosophy or sport, have a point for the sake of which they are pursued, and they can all be pursued for the sake of exchange-value as well or instead. When that happens, their own real point becomes a means to the end of exchange-value, which, being something quite different, transforms the activity and can threaten the real point and even destroy it. Aristotle is concerned, not only about the invasion by exchange-value of chrematistike, but about its invasion of ethical and political life as a whole. (pp. 178-179)

So we can now understand what I have called the most basic Marxian critique of capitalism— in capitalism the form of wealth getting that is ordered to increasing the quantity of exchange value has become dominant, subordinating the natural pursuit of use values to itself. As a result the concrete, useful labor naturally ordered to the creation of use-value, is subordinated to the abstract homogenous labor, which is the basis of exchange value. (I’m grateful to David Pederson for explaining this point to me). In such an economy competition ensures that forms of economic activity that do not do everything to maximize the increase of exchange value are quickly driven out of business. This also means that the conceptions of the good life promoted in a capitalist society are subordinated to selling goods. Instead of determining a-priori what is a good life, and then making things that help achieve it, capitalists invent and propagates any idea of the good life that will help them sell their products. Thus TV commercials are usually about how such and such a product is necessary to be ‘cool’ or ‘patriotic’ or ‘old-school’ or ‘up to date’ or whatever fake conception of the good life will induce people to buy the product.

But now let us compare this with pre-capitalist society. In an 1843 speech against repealing the Corn Laws Benjamin Disraeli argued as follows:

Now, what is the fundamental principle of the feudal system, gentlemen? It is that the tenure of all property shall be the performance of its duties. Why, when [William] the Conqueror carved out parts of the land, and introduced the feudal system, he said to the recipient, “You shall have that estate, but you shall do something for it: you shall feed the poor; you shall endow the Church; you shall defend the land in case of war; and you shall execute justice and maintain truth to the poor for nothing.” […] Why, when I hear a political economist, or an Anti-Corn-Law Leaguer, or some conceited Liberal reviewer come forward and tell us, as a grand discovery of modern science, twitting and taunting, perhaps, some unhappy squire who cannot respond to the alleged discovery — when I hear them say, as the great discovery of modern science, that “Property has its duties as well as its rights,” my answer is that that is but a feeble plagiarism of the very principle of that feudal system which you are always reviling. Let me next tell those gentlemen who are so fond of telling us that property has its duties as well as its rights, that labour also has rights as well as its duties; and when I see masses of property raised in this country which do not recognize that principle; when I find men making fortunes by a method which permits them (very often in a very few years) to purchase the lands of the old territorial aristocracy of the country, I cannot help remembering that those millions are accumulated by a mode which does not recognize it as a duty “to endow the Church, to feed the poor, to guard the land, and to execute justice for nothing.” And I cannot help asking myself, when I hear of all this misery, and of all this suffering; when I know that evidence exists in our Parliament of a state of demoralisation in the once happy population of this land, which is not equalled in the most barbarous countries, which we suppose the more rude and uncivilised in Asia are — I cannot help suspecting that this has arisen because property has been permitted to be created and held without the performance of its duties.

Clearly the economic system that Disraeli is here describing is one in which use value predominated over exchange value. In fact, it was primarily a system of distribution rather than of exchange. Goods were produced for the land owners, and then distributed by them according to an aristocratic, hierarchical conception of distributive justice. Now, Disraeli’s vision of the feudal system was certainly an idealized one, but it was a vision of a system of which strong traces were still left in his day. But those traces were about to be erased, and the 1846 repeal of the Corn Laws was a key step in that erasure. Of course, the victory of capitalism over ‘feudal’ society had begun much earlier with the dissolution of the monasteries and the ‘primitive accumulation’ and agricultural revolution that the dissolution enabled. But there was still a landed aristocracy that carried on something of the old form of life. The history of England from the Reformation to 1846 was largely determined by the struggle between capitalists and landed gentry with the Civil War being an early climax. But I would argue that in England the scale did not tip irrevocably toward the capitalist side till 1846.

Disraeli certainly predicted such a shift:

I want to ask the gentlemen who are members of the Anti-Corn-Law League, the gentlemen who are pressing on the Government of the country, on the present occasion, the total repeal and abolition of the Corn Laws […] I want them to consider this most important point […] how far the present law of succession and inheritance in land will survive the whole change of your agricultural policy? If that does not survive—if that falls—if we recur to the Continental system of parcelling out landed estates— I want to know how long you can maintain the political system of the country ? That estate of the Church which I mentioned; that estate of the poor to which I referred; that great fabric of judicial rights to which I made allusion; those traditionary manners and associations which spring out of the land, which form the national character, which form part of the possession of the poor not to be despised, and which is one of the most important elements of political power— they will tell you ‘Let it go!’ My answer to that is, ‘If it goes, it is a revolution, a great, a destructive revolution,’ and it is not my taste to live in an age of destructive revolution. (pp. 52-53)

Sixty years later, with the advantage of hindsight, Lord Cantilupe, the fictional High Tory in G. Lowes Dickinson’s A Modern Symposium makes the same argument:

Even after the first Reform Act—which, in my opinion was conceived upon the wrong lines—the landed gentry still governed England; and if I could have had my way they would have continued to do so. It wasn’t really parliamentary reform that was wanted; it was better and more intelligent government. And such government the then ruling class was capable of supplying, as is shown by the series of measures passed in the thirties and forties, the new Poor Law and the Public Health Acts and the rest. Even the repeal of the Corn Laws shows at least how capable they were of sacrificing their own interests to the nation; though otherwise I consider that measure the greatest of their blunders. I don’t profess to be a political economist, and I am ready to take it from those whose business it is to know that our wealth has been increased by Free Trade. But no one has ever convinced me, though many people have tried, that the increase of wealth ought to be the sole object of a nation’s policy. And it is surely as clear as day that the policy of Free Trade has dislocated the whole structure of our society. It has substituted a miserable city-proletariat for healthy labourers on the soil; it has transferred the great bulk of wealth from the country-gentleman to the traders; and in so doing it has more and more transferred power from those who had the tradition of using it to those who have no tradition at all except that of accumulation. The very thing which I should have thought must be the main business of a statesman—the determination of the proper relations of classes to one another—we have handed over to the chances of competition. We have abandoned the problem in despair, instead of attempting to solve it; with the result, that our population—so it seems to me—is daily degenerating before our eyes, in physique, in morals, in taste, in everything that matters; while we console ourselves with the increasing aggregate of our wealth. (pp. 10-11)

Cantilupe is in favor of an aristocratic society, and unlike Marx he doesn’t think it exploitative; he admires the peasants who work for him, and laments the fact that capitalism is abolishing their way of life:

There will be fewer of the kind of people in whom I take pleasure, whom I like to regard as peculiarly English, and who are the products of the countryside; fellows who grow like vegetables, and, without knowing how, put on sense as they put on flesh by an unconscious process of assimilation; who will stand for an hour at a time watching a horse or a pig, with stolid moon-faces as motionless as a pond; the sort of men that visitors from town imagine to be stupid because they take five minutes to answer a question, and then probably answer by asking another; but who have stored up in them a wealth of experience far too extensive and complicated for them ever to have taken account of it. They live by their instincts not their brains; but their instincts are the slow deposit of long years of practical dealings with nature. That is the kind of man I like. And I like to live among them in the way I do—in a traditional relation which it never occurs to them to resent, any more than it does to me to abuse it. That sort of relation you can’t create; it has to grow, and to be handed down from father to son. (pp. 13-14)

He loves hierarchical order:

I like a society properly ordered in ranks and classes. I like my butcher or my gardener to take off his hat to me, and I like, myself, to stand bareheaded in the presence of the Queen. I don’t know that I’m better or worse than the village carpenter; but I’m different; and I like him to recognize that fact, and to recognize it myself. (p 7-8)

And therefore he is against the rule of shopkeepers:

I believe that the pursuit of wealth tends to unfit men for the service of the state. And I sympathize with the somewhat extreme view of the ancient world that those who are engaged in trade ought to be excluded from public functions. I believe in government by gentlemen; and the word gentleman I understand in the proper, old-fashioned English sense, as a man of independent means, brought up from his boyhood in the atmosphere of public life, and destined either for the army, the navy, the Church, or Parliament. It was that kind of man that made Rome great, and that made England great in the past; and I don’t believe that a country will ever be great which is governed by merchants and shopkeepers and artisans. (p 9)

Cantilupe’s Toryism is indeed a far cry from the modern variety, whose heroine, Margaret Thatcher, was literally a grocer’s daughter. I find Cantilupe’s politics highly sympathetic, but in England his cause has now been a lost cause for a very long time. He laments that his way of life is dying out, and in the 20th century it did indeed die out almost completely. For a time some English aristocrats were able to replicate it in the colonies. Evelyn Waugh describes such replication in Kenya:

It is not big business enterprise which induces the Kenya settlers to hang on to their houses and lands, but the more gentle motive of love for a very beautiful country that they have come to regard as their home, and the wish to transplant and perpetuate a habit of life traditional to them, which England has ceased to accommodate— the traditional life of the English squirearchy, which, while it was still dominant, formed the natural target for satirists of every shade of opinion, but to which now that it has become a rare and exotic survival, deprived of the normality which was one of its determining characteristics, we can as a race look back with unaffected esteem and regret. I am sure that, if any of them read this book, they will deny with some embarrassment this sentimental interpretation of their motives. It is part of the very vitality of their character that they should do so. They themselves will say simply that farming was impossible in England, so they came to Kenya, where they understood that things were better; they will then grouse a little about the government, and remark that after all, bad as things are, it is still possible to keep a horse or two and get excellent shooting— things only possible at home for those who spend the week in an office. That would be their way of saying what I have just said above. (Waugh Abroad, p. 323)

The Kenyan squirearchy was beautiful described by Elspeth Huxley in The Flame Trees of Thika, but it too soon perished.

Cantilupe’s way of life is now thoroughly lost, and there is no political force trying to restore it. There is however a certain amount of nostalgia for that way of life. Witness the extremely popular ITV costume drama Downton Abbey. I find it darkly funny that in our day the first thing that springs to mind to illustrate the longing for the days of Cantilupe is a TV show. In the ‘iron cage’ of capitalism (to use Max Weber’s expression) even nostalgia for a pre-capitalist society is exploited by capitalist TV companies to make money.

When Pete Buttigieg accepted a position at the management consultancy McKinsey & Company, he already had sterling credentials: high-school valedictorian, a bachelor’s degree from Harvard, a Rhodes Scholarship. He could have taken any number of jobs and, moreover, had no obvious interest in business. Nevertheless, he joined the firm.

This move was predictable, not eccentric: The top graduates of elite colleges typically pass through McKinsey or a similar firm before settling into their adult career. But the conventional nature of the career path makes it more, not less, worthy of examination. How did this come to pass? And what consequences has the rise of management consulting had for the organization of American business and the lives of American workers?

The answers to these questions put management consultants at the epicenter of economic inequality and the destruction of the American middle class. The answers also explain why the Democratic Party’s left wing is so suspicious of the nice and obviously impressive young man who wishes to be president.

Management consultants advise managers on how to run companies; McKinsey alone serves management at 90 of the world’s 100 largest corporations. Managers do not produce goods or deliver services. Instead, they plan what goods and services a company will provide, and they coordinate the production workers who make the output. Because complex goods and services require much planning and coordination, management (even though it is only indirectly productive) adds a great deal of value. And managers as a class capture much of this value as pay. This makes the question of who gets to be a manager extremely consequential.

More by Daniel Markovits

In the middle of the last century, management saturated American corporations. Every worker, from the CEO down to production personnel, served partly as a manager, participating in planning and coordination along an unbroken continuum in which each job closely resembled its nearest neighbor. Elaborately layered middle managers—or “organization men”—coordinated production among long-term employees. In turn, companies taught workers the skills they needed to rise up the ranks. At IBM, for example, a 40-year worker might spend more than four years, or 10 percent, of his work life in fully paid, IBM-provided training.

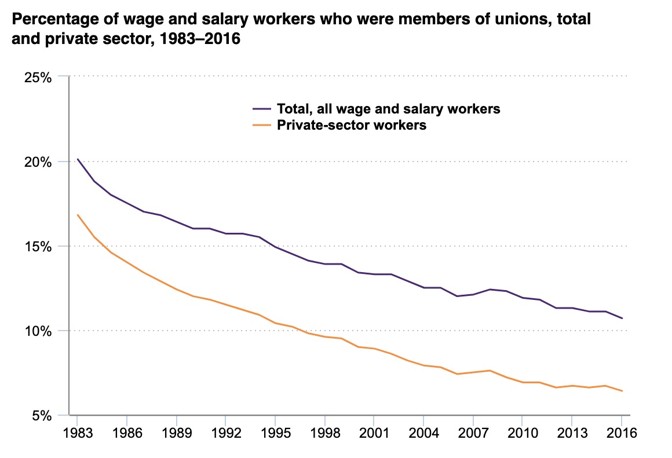

Mid-century labor unions (which represented a third of the private-sector workforce), organized the lower rungs of a company’s hierarchy into an additional control center—as part of what the United States Supreme Court, writing in 1960, called “industrial self-government”—and in this way also contributed to the management function. Even production workers became, on account of lifetime employment and workplace training, functionally the lowest-level managers. They were charged with planning and coordinating the development of their own skills to serve the long-run interests of their employers.

The mid-century corporation’s workplace training and many-layered hierarchy built a pipeline through which the top jobs might be filled. The saying “from the mail room to the corner office” captured something real, and even the most menial jobs opened pathways to promotion. In 1939, for example, all save two of the grocery chain Safeway’s division managers had started their careers behind the checkout counter. At McDonalds, Ed Rensi worked his way up from flipping burgers in the 1960s to become CEO. More broadly, a 1952 report by Fortune magazine found that two-thirds of senior executives had more than 20 years’ service at their current companies.

Middle managers, able to plan and coordinate production independently of elite-executive control, shared not just the responsibilities but also the income and status gained from running their companies. Top executives enjoyed commensurately less control and captured lower incomes. This democratic approach to management compressed the distribution of income and status. In fact, a mid-century study of General Motors published in the Harvard Business Review—completed, in a portent of what was to come, by McKinsey’s Arch Patton—found that from 1939 to 1950, hourly workers’ wages rose roughly three times faster than elite executives’ pay. The management function’s wide diffusion throughout the workforce substantially built the mid-century middle class.

At the time of Patton’s study, McKinsey and other management consultants still played a relatively minor role in how American companies were run. The earliest consultants were engineers who advised factory owners on measuring and improving efficiency at the complex factories required for industrial production. The then-leading firm, Booz Allen, did not achieve annual revenues of $2 million until after the Second World War. McKinsey, which didn’t hire its first Harvard M.B.A. until 1953, retained a diffident and traditional ethos—requiring its consultants to wear fedoras until President John F. Kennedy stopped wearing his.

Things changed in the 1960s, with McKinsey leading the way. In 1965 and 1966, the firm placed help-wanted ads in The New York Times and Time magazine, with the goal of generating applications that it could then reject, to establish its own eliteness. McKinsey’s competitors followed suit, as when the Boston Consulting Group’s Bruce Henderson took out ads in the Harvard Business School student newspaper seeking to hire “not just the run-of-that-mill but, instead, scholars—Rhodes Scholars, Marshall Scholars, Baker Scholars (the top 5 percent of the class).”

A new ideal of shareholder primacy, powerfully championed by Milton Friedman in a 1970 New York Times Magazine article entitled “The Social Responsibility of Business is to Increase its Profits,” gave the newly ambitious management consultants a guiding purpose. According to this ideal, in language eventually adopted by the Business Roundtable, “the paramount duty of management and of boards of directors is to the corporation’s stockholders.” During the 1970s, and accelerating into the ’80s and ’90s, the upgraded management consultants pursued this duty by expressly and relentlessly taking aim at the middle managers who had dominated mid-century firms, and whose wages weighed down the bottom line.

As the business journalist Walter Kiechel put it in his book Lords of Strategy, consultants openly sought to “foment a stratification within companies and society” by concentrating the management function in elite executives, aided (of course) by advisers from consultants’ own ranks. Management-consulting firms deployed a panoply of branded processes against middle management. Another account of the industry, The Witch Doctors, explains that the Computer Sciences Corporation’s consulting arm, working with the Sloan School of Management at MIT, developed corporate “reengineering” to “break an organization down into its components parts,” eliminate the redundant ones, namely middle managers, and then put the remaining parts “together again to create a new machine.” GTE, Apple, and Pacific Bell would all cite reengineering as responsible for their downsizing. McKinsey framed its path to downsizing, which the firm called “overhead value analysis,” as an answer to the mid-century corporation’s excessive reliance on middle management. As McKinsey’s John Neuman admitted in an essay introducing the method, the “process, though swift, is not painless. Since overhead expenses are typically 70% to 85% people-related and most savings come from work-force reductions, cutting overhead does demand some wrenching decisions.”

Management consultants thus implemented and rationalized a transformation in the American corporation. Companies that had long affirmed express “no layoff” policies now took aim at what the corporate raider Carl Icahn, writing in the The New York Times in the late 1980s, called “corporate bureaucracies” run by “incompetent” and “inbred” middle managers. They downsized in response not to particular business problems but rather to a new managerial ethos and methods; they downsized when profitable as well as when struggling, and during booms as well as busts. The downsizing peaked during the extraordinary economic boom of the 1990s. The culls, moreover, were dramatic. AT&T, for example, once aimed to cut the ratio of managers to nonmanagers in one of its units from 1:5 to 1:30. Overall, middle managers were downsized at nearly twice the rate of nonmanagerial workers. Downsizing was indeed wrenching. When IBM abandoned lifetime employment in the 1990s, local officials asked gun-shop owners around its headquarters to close their stores while employees absorbed the shock.

Production workers did not escape the whirlwind, as companies—again with help from consultants— stripped them of their residual management functions and the benefits that these sustained. Corporations broke their unions, and jobs that once carried bright futures became gloomy. United Parcel Service, long famous for emphasizing full-time workers and promoting from within, shifted to part-time work in 1993. Its union—the Teamsters—struck in 1997, under the slogan “Part-time America won’t work,” but lost the strike. UPS has since hired more than half a million part-time workers, with just 13,000 advancing within the company.

Overall, the share of private-sector workers belonging to a union fell from about one-third in 1960 to less than one-sixteenth in 2016. In some cases, downsized employees have been hired back as subcontractors, with no long-term claim on the companies and no role in running them. When IBM laid off masses of workers in the 1990s, for example, it hired back one in five as consultants. Other corporations were built from scratch on a subcontracting model. The clothing brand United Colors of Benetton has only 1,500 employees but uses 25,000 workers through subcontractors.

The shift from permanent to precarious jobs continues apace. Buttigieg’s work at McKinsey included an engagement for Blue Cross Blue Shield of Michigan, during a period when it considered cutting up to 1,000 jobs (or 10 percent of its workforce). And the gig economy is just a high-tech generalization of the sub-contractor model. Uber is a more extreme Benetton; it deprives drivers of any role in planning and coordination, and it has literally no corporate hierarchy through which drivers can rise up to join management. As ever, consultants are at the forefront of change, aiming to disrupt the management function. A new breed of management-consulting firms now deploys algorithmic processing to automate not the line workers’ or sales associates’ jobs, but the manager’s job.

In effect, management consulting is a tool that allows corporations to replace lifetime employees with short-term, part-time, and even subcontracted workers, hired under ever more tightly controlled arrangements, who sell particular skills and even specified outputs, and who manage nothing at all.

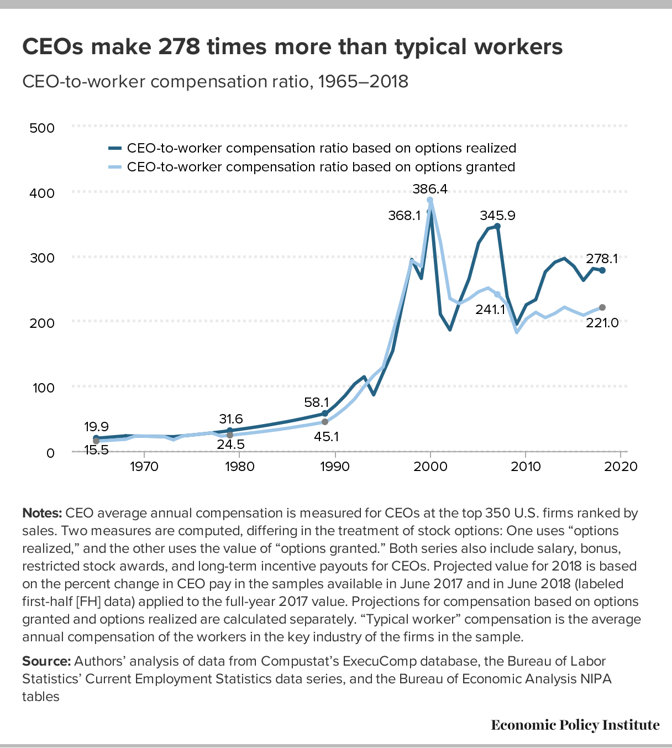

The management function has not been rendered unnecessary, of course, or disappeared. Instead, the managerial control stripped from middle managers and production workers has been concentrated in a narrow cadre of executives who monopolize planning and coordination. Mid-century, democratic management empowered ordinary workers and disempowered elite executives, so that a bad CEO could do little to harm a company and a good one little to help it. Today, top executives boast immense powers of command—and, as a result, capture virtually all of management’s economic returns. Whereas at mid-century a typical large-company CEO made 20 times a production worker’s income, today’s CEOs make nearly 300 times as much. In a recent year, the five highest-paid employees of the S&P 1500 (7,500 elite executives overall), obtained income equal to about 10 percent of the total profits of the entire S&P 1500.

Management consultants insist that meritocracy required the restructuring that they encouraged—that, as Kiechel put it dryly, “we are not all in this together; some pigs are smarter than other pigs and deserve more money.” Consultants seek, in this way, to legitimate both the job cuts and the explosion of elite pay. Properly understood, the corporate reorganizations were, then, not merely technocratic but ideological. Rather than simply improving management, to make American corporations lean and fit, they fostered hierarchy, making management, in David Gordon’s memorable phrase, “fat and mean.”

Running a company on a concentrated model requires a cadre of managers who possess the capacity and taste to work with the intensity demanded of top executives today. At the same time, corporate reorganizations have deprived companies of an internal supply of managerial workers. When restructurings eradicated workplace training and purged the middle rungs of the corporate ladder, they also forced companies to look beyond their walls for managerial talent—to elite colleges, business schools, and (of course) to management-consulting firms. That is to say: The administrative techniques that management consultants invented created a huge demand for precisely the services that the consultants supply.

This is where the recent history of American management intersects with Pete Buttigieg’s life story.

Whereas a century ago, fewer than one in five of America’s business leaders had completed college, top executives today typically have elite degrees—M.B.A.s as well as bachelor’s degrees—and deep ties to management consulting. Many executives have consulting backgrounds themselves. McKinsey alone counts 70 Fortune 500 CEOs among its alumni, including the current CEOs or COOs at Google, Facebook, and Morgan Stanley. Indeed, a greater share of McKinsey employees become CEOs than any other company’s in the world. Management consultants who stay with their firms also do very well. The three most elite management consultancies—McKinsey, Bain & Company, and the Boston Consulting Group—regularly boast double-digit revenue growth and today generate nearly $20 billion in revenues and employ nearly 50,000 people.

These facts give management consulting a powerful charisma for students and recent graduates of elite colleges and universities. Today, management consulting sits beside finance as the most popular first job for graduates of Harvard, Princeton, and Yale. (Stanford graduates choose among consulting, finance, and tech.) Harvard Business School, which sent zero graduates to McKinsey prior to 1953, now regularly sends nearly a quarter of its graduating class into consulting, while Wharton graduates are 10 times more likely to work in consulting than in manufacturing.

The incomes that management consultants secure renders these numbers unsurprising. McKinsey pays B.A.s nearly $100,000 and newly minted M.B.A.s nearly $200,000, and although the firm does not release information about profits, industry insiders believe that partners might command incomes in the millions. McKinsey’s charisma, however, is not just economic. The firm continues to perform its own eliteness, with the application process involving famously rigorous analytic interviews—which test formal problem-solving skills but no substantive knowledge (certainly not of any concrete industry or business)—so that getting hired has in itself become a mark of accomplishment at top colleges. McKinsey also continues aggressively to recruit the most elite graduates, treating Rhodes or Marshall Scholarships as equivalent to M.B.A.s for the purpose of rank and pay, and boasting, “We are the largest employers of Rhodes scholars and Marshall scholars on the planet, outside of the United States government.”

Meanwhile, the firm expressly emphasizes its internal meritocracy. McKinsey’s mission statement promises to “create an unrivaled environment for exceptional people” and the firm boasts of its “university-like capabilities,” which give its consultants proprietary analytic powers that no other business advisers can match. A recent survey of business-school graduates found that it demands longer hours than any employer of M.B.A.s other than Goldman Sachs and Barclays. And it embraces an “up or out” promotion regime, under which people who stop advancing through the firm are asked to leave.

Consulting, like law school, is an all-purpose status giver—“low in risk and high in reward,” according to the Harvard Crimson. McKinsey also hopes that its meritocratic excellence will legitimate its activities in the eyes of the broader world. Management consulting, Kiechel observed, acquired its power and authority not from “silver-haired industry experience but rather from the brilliance of its ideas and the obvious candlepower of the people explaining them, even if those people were twenty-eight years old.”

Pete Buttigieg fit the McKinsey profile perfectly. “I went to work at McKinsey because I wanted to understand how the world worked,” he has said, adding that “they were willing to take a chance on me even though I didn’t have an M.B.A.” He believes that the lessons the firm teaches apply widely, not just across industries but to government as well: In an interview with The Atlantic, he said that McKinsey was “a place where I could learn as much as I could by working on interesting problems and challenges in the private sector, the public sector, in the nonprofit sector.” Perhaps he was right. He became—without any prior governmental experience—the youngest mayor in South Bend’s history; and now he aspires to become—without ever having held national or even statewide office—the youngest president in American history.

Yet Buttigieg’s association with McKinsey also exacerbates the left’s skepticism of his candidacy. The firm’s clients—which include ICE, opioid manufacturers, and authoritarian regimes—generated the first doubtful headlines, as people wanted to know whether Buttigieg would disclose his McKinsey client list. Buttigieg answered, “I never worked on a project inconsistent with my values, and if asked to do so, I would have left the firm rather than participate.” He probably wouldn’t have had to leave, because McKinsey allows its employees to refuse to work for particular clients that they regard as unconscionable. It is therefore no surprise that when Buttigieg eventually did disclose his clients, the companies were indeed benign.

A deeper objection to Buttigieg’s association with McKinsey concerns not whom the firm represents but the central role the consulting revolution has played in fueling the enormous economic inequalities that now threaten to turn the United States into a caste society.