Drug Pricing

Drug Pricing

A Look at Recent Proposals to Control Drug Spending by Medicare and its Beneficiaries (Kaiser Family Foundation, Aug 01, 2019)

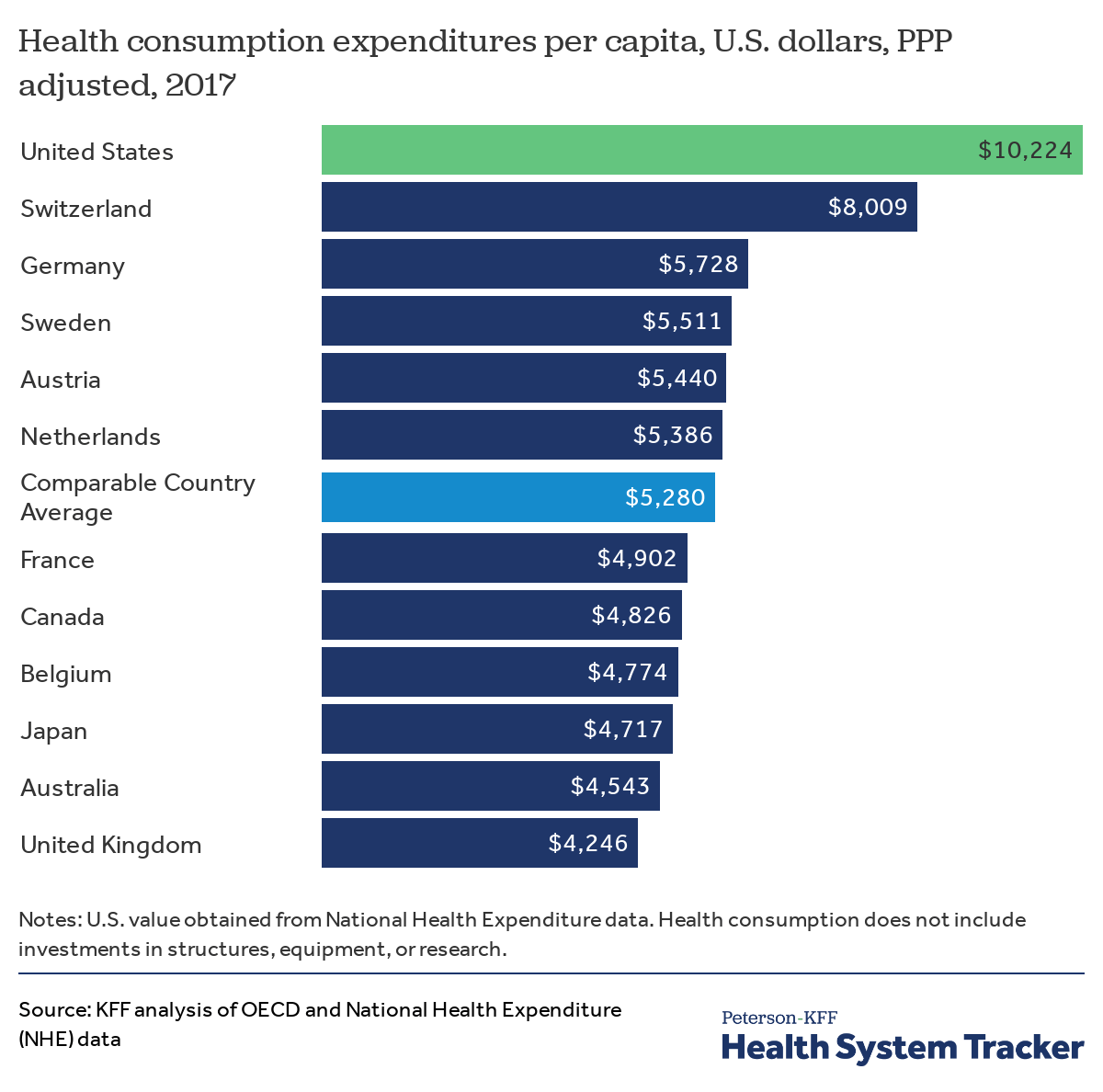

The affordability of prescription drugs is a pressing concern for many Americans, with broad agreement across the political spectrum that lowering prescription drug costs should be a top priority for Congress. The Trump Administration, members of Congress, and several 2020 presidential candidates have offered proposals to lower drug prices. Many of these proposals would affect prescription drug spending under Medicare, which accounts for 30 percent of national retail spending on drugs and nearly $1 out of every $5 in total Medicare spending (Figure 1).

Prescription drugs are an important component of health care for Medicare beneficiaries, which includes more than 60 million older adults and people with long-term disabilities. The majority of Medicare prescription drug spending is for drugs covered under Part D, the outpatient prescription drug benefit. Medicare Part B also covers drugs that are administered to patients in physician offices and other outpatient settings.

Medicare lets private payers negotiate on their behalf. Medicare outsources the negotiation process to private payers. For drugs bought in pharmacies, these drugs are paid under Part D insurance plans. Seniors purchase Part D plans from private payers who contract with Medicare to provide this insurance. For drugs administered by a doctor, Medicare will average the drug prices negotiated across all private payers. This is called the “Average Selling Price.” or ASP which also dictates how doctor’s get paid for drug-related services. Medicare reimburses doctors ASP + 4.3% for doctor-administered drugs.

Medicaid and VA Drug Pricing

Medicaid takes the lowest negotiated price by private payers. After which, states have the right to further negotiate price. Aetna, Express Scripts, and Oscar Insurance all negotiate with pharma companies for the best price. Perhaps Aetna and Oscar only receive 20% discounts while Express Scripts receives a 30% discount. This 30% discounted price is now the Medicaid price. Additional requirements ensure this price level adjusts to inflation. Although the federal government helps fund Medicaid, it’s managed at the state level. At the state level, Medicaid can indeed negotiate further discounts with pharmaceutical companies. However, the federal government is still prohibited.

For Medicaid, companies are mandated to provide drug price rebates.

For

The Veterans Administration (VA) drug companies must charge the lowest price they offer to anyone in the private sector. The VA is also entitled to a guaranteed minimum discount of 24 percent off the non-federal Average Manufacturer Price (an amount similar to the minimum discount guaranteed to Medicaid), or a lower price to match the best price provided to non-federal purchasers.

The 1992 Veterans Health Care Act granted the VA minimum discounts on drugs, similar to those received by Medicaid. Notably, the VA discount was enacted after the 1990 Medicaid rebate law, which guaranteed Medicaid a discounted price and also required manufacturers to give Medicaid the "best price" they offered. Once the Medicaid rebate law took effect, some manufacturers canceled discounts to other purchasers (including the VA) to avoid setting a best price that would also have to be offered to Medicaid.

In 2000 the GAO found that one likely impact of extending VA or Medicaid pricing to the Medicare population would be an increase in prices for federal and private purchasers. Citing the experience after enactment of the Medicaid rebate law, the GAO stated that manufacturers would likely cancel other federal pricing agreements wherever possible to avoid having to extend those prices to the much larger Medicare population.

Congress has lowered the percentage doctors may get with the ASP which then lowered drug costs for Medicare. But the processes for drug pricing for the VA, Medicaid, and Medicare are established by law. Since drug pricing for Medicare is determined by ASP vs lowest negotiated price and rebates for Medicaid, Medicare prices are higher.

A Medicaid for All would be cheaper than Medicare for All unless under new law Medicare drug pricing were changed to lowest negotiated price. But drug companies would examine canceling other contracts to keep prices higher. Only in the case where the federal government was the only health care purchaser and negotiator would this type of move by drug companies be negated. Other proposed ways of lowering drug costs to the consumer outside of statutory changes to Medicare and Medicaid laws are reviewed in the article above.

In 2017, total gross spending on prescription drugs was $154.9 billion in Medicare Part D, $30.4 billion in Part B, and $67.6 billion in Medicaid.