You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

stock market/financial ?'s

- Thread starter PANDFAN

- Start date

jimmymac

Well-known member

- Messages

- 1,566

- Reaction score

- 242

This chart in Ackerman's class really lit a fire under my ***.

A Fully-Funded Roth IRA At Age 18 Could Net You 3.5 Million Dollars - No Credit Needed

The more you save at a younger age, the more you have for the future. Save big and live a normal life instead of buying that new piece of technology and you can really get your money's worth later in life.

I am also a fan of PIMCO and VANGUARD funds. Steer clear of most things with a management fee.

I get my first Ackermann test back tomorrow. Hope it goes well

BleedBlueGold

Well-known member

- Messages

- 6,300

- Reaction score

- 2,515

This chart in Ackerman's class really lit a fire under my ***.

A Fully-Funded Roth IRA At Age 18 Could Net You 3.5 Million Dollars - No Credit Needed

The more you save at a younger age, the more you have for the future. Save big and live a normal life instead of buying that new piece of technology and you can really get your money's worth later in life.

I am also a fan of PIMCO and VANGUARD funds. Steer clear of most things with a management fee.

You can actually open a Roth earlier than 18 if you're earning an income.

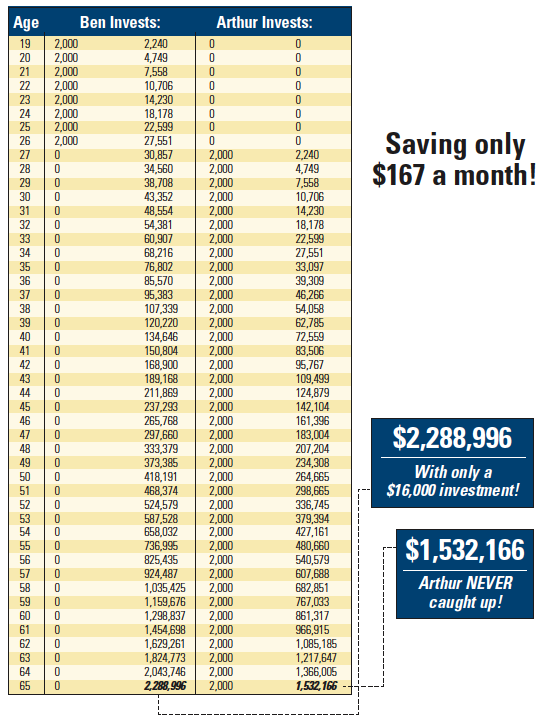

I personally like the Ben & Arthur example:

Bottom line...start saving/investing as early as possible in life and don't touch it until you're ready to retire. "Life" will happen, but if you live on a budget and have a cash-funded emergency net, you'll be able to dodge those crises.

Panda:

make sure you have life insurance.

you have 4 kids and a wife.

get it and get it now.

get term life, nothing else.

(your wife should get some too)

Very good advice. My wife and I just got ours. Contact Zander Insurance for the best rates. It's suggested that you get 10-12 times your annual income and the term should be 15-20 years (or until you feel like you can be self-insured). We chose a 30-year term only because we're still young and don't have kids yet.

PANDFAN

Look Down

- Messages

- 16,771

- Reaction score

- 2,278

life insurance has been thrown out there...by the way i love the david ramsey model..thanks!!

what are the benefits right now for having life insurance vs if we wait a couple of years??...my wife has an insurance policy at work which she doesn't have to contribute to, but does have her own outside of this...she was thinking of cashing this in as a way of allowing us to get that "emergency fund set up"

what are the benefits right now for having life insurance vs if we wait a couple of years??...my wife has an insurance policy at work which she doesn't have to contribute to, but does have her own outside of this...she was thinking of cashing this in as a way of allowing us to get that "emergency fund set up"

GET THIS BOOK AND LISTEN TO NOBODY ELSE'S ADVISE.

+1. Best, and more importantly, the most realistic, book on investing.

pumpdog20

Well-known member

- Messages

- 4,760

- Reaction score

- 3,196

Yeah, pumpdog's got it. Dave's most well known book is The Total Money Makeover, which outlines those steps as well as provides simple worksheets to setup your budget. If you don't want to buy the book, just search for his spreadsheets online, you can get excel files very similar to his plan, although I recommend at least gettign the book so you understand what his methods are based on. He also has another book called Financial Peace that is similar. Dave's philospohy is Christian-based, so many churches offer his "group budgeting" program called Financial Peace University. If you get his book and spreadsheets, it's probably not necessary to do FPU. In my opinion FPU is more geared as a support group for folks who are new to budgeting and are in some significant debt looking for a way out of it. Dave also has a radio show too, but he tends to get a little carried away on it with marketing his products IMO.

Listen to the day old podcast and skip the commercials, best way to go.

BleedBlueGold

Well-known member

- Messages

- 6,300

- Reaction score

- 2,515

life insurance has been thrown out there...by the way i love the david ramsey model..thanks!!

what are the benefits right now for having life insurance vs if we wait a couple of years??...my wife has an insurance policy at work which she doesn't have to contribute to, but does have her own outside of this...she was thinking of cashing this in as a way of allowing us to get that "emergency fund set up"

The reason for getting life insurance is the same reason you'd get car insurance or home insurance, etc. It's for peace of mind. Knowing my wife and eventual kids will still be ok if something happens to me is more than enough reason to get it. Term life is very affordable. Example: $750,000 30-year policy is about $50 per month (give or take based on personal health).

The reasoning for getting 10x your salary is that your spouse can invest that check into a good mutual fund portfolio with a target goal of 10%. She can then live off the 10% growth, which would equal your income had you still been alive. In short, it's income-replacement insurance.

I'm not an expert so I'm not sure about cashing in a current policy. Dave Ramsey has some Insurance ELP's as well. I'm sure they'd be happy to help with any questions in that regard.

Keep in mind that there are plenty of other types of life insurance policies out there. They all have their pros and cons. However, Dave's main points on Term life is that it's cheap enough to give you that peace of mind and still leave you with plenty of money left over to use towards investing. Ideally, when you retire, you shouldn't need the life insurance anymore because you will have a nest egg big enough to cover a death.

Ndaccountant

Old Hoss

- Messages

- 8,381

- Reaction score

- 5,789

life insurance has been thrown out there...by the way i love the david ramsey model..thanks!!

what are the benefits right now for having life insurance vs if we wait a couple of years??...my wife has an insurance policy at work which she doesn't have to contribute to, but does have her own outside of this...she was thinking of cashing this in as a way of allowing us to get that "emergency fund set up"

All I will say is this:

Last year my sister and brother in-law's neighbor died suddenly and unexpectedly. He was under 40 years old and left behind a wife a 3 kids under the age 12. He did not have any life insurance. Within six months, they had to sell the house and move to an apartment.They had to liquidate some of their retirement savings and college funds to pay for the funeral. Luckily, the school and community had a huge fundraiser for the family and was able to raise about $100k for them, but much of that went towards selling the house and finding a new place to live while the wife looked for employment.

Life insurance is absolutely needed to ensure that your family could maintain their standard of living in the face of the unthinkable. Additionally, I would recommend having life insurnace on your kids as well. I have two people that had to deal with the nightmare of losing a child and took time away from work to grieve. They had insurance to protect them from funeral costs and lost wages due to time away from work.

Last edited:

Ndaccountant

Old Hoss

- Messages

- 8,381

- Reaction score

- 5,789

The reason for getting life insurance is the same reason you'd get car insurance or home insurance, etc. It's for peace of mind. Knowing my wife and eventual kids will still be ok if something happens to me is more than enough reason to get it. Term life is very affordable. Example: $750,000 30-year policy is about $50 per month (give or take based on personal health).

The reasoning for getting 10x your salary is that your spouse can invest that check into a good mutual fund portfolio with a target goal of 10%. She can then live off the 10% growth, which would equal your income had you still been alive. In short, it's income-replacement insurance.

I'm not an expert so I'm not sure about cashing in a current policy. Dave Ramsey has some Insurance ELP's as well. I'm sure they'd be happy to help with any questions in that regard.

Keep in mind that there are plenty of other types of life insurance policies out there. They all have their pros and cons. However, Dave's main points on Term life is that it's cheap enough to give you that peace of mind and still leave you with plenty of money left over to use towards investing. Ideally, when you retire, you shouldn't need the life insurance anymore because you will have a nest egg big enough to cover a death.

True. Additionally, when you retire, you no longer have the financial obligations that you did when you were younger.

BleedBlueGold

Well-known member

- Messages

- 6,300

- Reaction score

- 2,515

All I will say is this:

Last year my sister and brother in-law's neighbor died suddenly and unexpectedly. He was under 40 years old and left behind a wife a 3 kids under the age 12. He did not have any life insurance. Within six months, they had to sell the house and move to an apartment.They had to liquidate some of their retirement savings and college funds to pay for the funeral. Luckily, the school and community had a huge fundraiser for the family and was able to raise about $100k for them, but much of that went towards selling the house and finding a new place to live while the wife looked for employment.

Life insurance is absolutely needed to ensure that your family could maintain their standard of living in the face of the unthinkable. Additionally, I would recommend having life insurnace on your kids as well. I have two people that had to deal with the nightmare of losing a child and took time away from work to grieve. They had insurance to deal protect them from funeral costs and lost wages due to time away from work.

I've always been told to not waste the money on carrying life insurance for kids, but this is a very good argument for doing so. I've actually never thought of it that way. Thanks for providing a different angle.

irishpat183

Banned

- Messages

- 5,625

- Reaction score

- 504

This chart in Ackerman's class really lit a fire under my ***.

A Fully-Funded Roth IRA At Age 18 Could Net You 3.5 Million Dollars - No Credit Needed

The more you save at a younger age, the more you have for the future. Save big and live a normal life instead of buying that new piece of technology and you can really get your money's worth later in life.

I am also a fan of PIMCO and VANGUARD funds. Steer clear of most things with a management fee.

I started mine at 24...little late, but tax free money on the way out is worth every penny I don't blow on beer and game tickets now.

irishpat183

Banned

- Messages

- 5,625

- Reaction score

- 504

life insurance has been thrown out there...by the way i love the david ramsey model..thanks!!

what are the benefits right now for having life insurance vs if we wait a couple of years??...my wife has an insurance policy at work which she doesn't have to contribute to, but does have her own outside of this...she was thinking of cashing this in as a way of allowing us to get that "emergency fund set up"

I have my life and health license if you want to PM me,. I'll be happy to help you out.

BleedBlueGold

Well-known member

- Messages

- 6,300

- Reaction score

- 2,515

True. Additionally, when you retire, you no longer have the financial obligations that you did when you were younger.

Exactly.

To further build on Term Life pros, some will argue that Whole Life provides a "forced savings account" and it can be used as an investment that will eventually cover the cost of your premium. They also can be used in estate planning.

1) I'm pretty sure that only the death benefit will be paid out and the savings vanishes in most cases.

2) Whole Life policies are very very expensive compared to Term Life. Yes, some of that monthly payment goes into the savings account, but the growth on said account is minimal. Do not use these types of policies as your primary investment accounts.

3) If your only reason for getting Whole Life is the estate planning/tax sheltered benefits, why not just find an attorney that can plan your estate w/o the high cost of a bad life insurance policy?

I don't mean to turn this into a debate on which insurance policy is better. The bottom line, as NDaccountant said, is that you need it and waiting shouldn't be an option. You never know what might happen.

irishpat183

Banned

- Messages

- 5,625

- Reaction score

- 504

Exactly.

To further build on Term Life pros, some will argue that Whole Life provides a "forced savings account" and it can be used as an investment that will eventually cover the cost of your premium. They also can be used in estate planning.

1) I'm pretty sure that only the death benefit will be paid out and the savings vanishes in most cases.

2) Whole Life policies are very very expensive compared to Term Life. Yes, some of that monthly payment goes into the savings account, but the growth on said account is minimal. Do not use these types of policies as your primary investment accounts.

3) If your only reason for getting Whole Life is the estate planning/tax sheltered benefits, why not just find an attorney that can plan your estate w/o the high cost of a bad life insurance policy?

I don't mean to turn this into a debate on which insurance policy is better. The bottom line, as NDaccountant said, is that you need it and waiting shouldn't be an option. You never know what might happen.

Whole life creates a "pay as you go" in many cases, therefore, you're not bound to premiums if you can't pay it.

Also, it's accumulating tax deferred in the cash account, and pays out a tax free death benny.

The problem with term is that premiums are lost and coverage expires if you outlive the term. Although, with younger folks the prems are cheap, therefore an inexpensive option.

Irish Houstonian

New member

- Messages

- 2,722

- Reaction score

- 301

I personally don't like Whole Life either really, but if you are looking for like a 30 or 40 year insurance policy, WL is usually the way to go rather than all the term life rate increases.

BleedBlueGold

Well-known member

- Messages

- 6,300

- Reaction score

- 2,515

I personally don't like Whole Life either really, but if you are looking for like a 30 or 40 year insurance policy, WL is usually the way to go rather than all the term life rate increases.

Pretty sure you're locked in to the premiums for the length of the term. 30-year terms are available. Most people shouldn't need anything beyond 30 years. They should have their nest egg established by then. Whole Life is very expensive and limits your ability to invest in better areas.

NDFANnSouthWest

We are ND!

- Messages

- 4,806

- Reaction score

- 199

My Two Cents:

Get out of debt (school loans, CC,), now there is some debt that is really hard to get out of like mortgage and day to day expenses. Once you pay one CC then take that $ and apply it to the next debt and so on.

Put a budget together. This is essential to living within/below your means.

Don't impulse buy, this gets alot of ppl in trouble. Remember to approach financials with a level non-emotions head.

My approach to CC is we use it day to day for fuel/groceries and at the end of the month pay it in full. This keeps you building a positive credit score with some flexibility for emergencies. Also note that if someones steals your CC and runs up a bill you are protected however on a debt card you are sol.

Hide your $ legally. Max out your 401k (set at $17500 for a family) also if your company has a High Deductible Health Plan, all the money you put in is pre tax dollars (max of $6450). So you have a potential of $23,950 tax shelter.

Get out of debt (school loans, CC,), now there is some debt that is really hard to get out of like mortgage and day to day expenses. Once you pay one CC then take that $ and apply it to the next debt and so on.

Put a budget together. This is essential to living within/below your means.

Don't impulse buy, this gets alot of ppl in trouble. Remember to approach financials with a level non-emotions head.

My approach to CC is we use it day to day for fuel/groceries and at the end of the month pay it in full. This keeps you building a positive credit score with some flexibility for emergencies. Also note that if someones steals your CC and runs up a bill you are protected however on a debt card you are sol.

Hide your $ legally. Max out your 401k (set at $17500 for a family) also if your company has a High Deductible Health Plan, all the money you put in is pre tax dollars (max of $6450). So you have a potential of $23,950 tax shelter.

Ndaccountant

Old Hoss

- Messages

- 8,381

- Reaction score

- 5,789

Pretty sure you're locked in to the premiums for the length of the term. 30-year terms are available. Most people shouldn't need anything beyond 30 years. They should have their nest egg established by then. Whole Life is very expensive and limits your ability to invest in better areas.

Agree. The premiums you pay in excess of term life need to be measured against the rate of return you could get on that money if deployed elsewhere. In some instances, WL is very useful. In others, it ends up costing you more in the end. It truly is up to the individual situation tho.

- Messages

- 20,894

- Reaction score

- 8,126

Surprised wooly hasn't weighed in on this yet.

Irish Houstonian

New member

- Messages

- 2,722

- Reaction score

- 301

You can get 30 year terms, but imo the combination of no cash value versus lapse risk isn't worth the difference. YRMV

RallySonsOfND

All-Snub Team Snubbed

- Messages

- 2,106

- Reaction score

- 91

My parents both have whole life, as well as myself. The amount the policy is worth depends on the amount paid into. I can continue with the payments myself when I graduate to increase the amount it is worth or leave it as is. The great part about our policy is no matter what, your family will receive a nice chunk of change no matter what.

RallySonsOfND

All-Snub Team Snubbed

- Messages

- 2,106

- Reaction score

- 91

Surprised wooly hasn't weighed in on this yet.

Isn't he commercial banking not investment?

BleedBlueGold

Well-known member

- Messages

- 6,300

- Reaction score

- 2,515

You can get 30 year terms, but imo the combination of no cash value versus lapse risk isn't worth the difference. YRMV

1) There shouldn't be any risk once your term expires if you've invested the difference. Your nest egg will be there to take care of you. You won't need a WL policy at that point.

2) Investing the difference in savings from a TL vs WL into a good growth mutual fund would far exceed any cash value developed over the course of your WL policy.

Example: A 40 yr old woman could get a $500K WL insurance policy for about $4200 a year. That same woman could get a 30-yr, $500K TL insurance policy for about $480 a year. If she invested the difference ($3720) every year during that 30 year term, her nest egg would be worth over $700K when it expired (based on 30 years at 10% growth...yes, there are funds that avg 10% since inception). To take it a little further, she could stop investing at that point and let her nest egg grow over the next 15 years until she passes away at the age of 85. At that point a WL policy would pay her beneficiary $500k. (Feel free to prove me wrong, but I have yet to come across a WL policy that pays the beneficiary the Death Benefit AND the accumulated savings over that person's life.) Where as route 2 pays her beneficiary $3 million (For those not following...that $700K will continue to grow at 10% for the next 15 years, ultimately being worth over $3M).

1,000th post!!

Irish Houstonian

New member

- Messages

- 2,722

- Reaction score

- 301

1) There shouldn't be any risk once your term expires if you've invested the difference. Your nest egg will be there to take care of you. You won't need a WL policy at that point.

2) Investing the difference in savings from a TL vs WL into a good growth mutual fund would far exceed any cash value developed over the course of your WL policy.

Example: A 40 yr old woman could get a $500K WL insurance policy for about $4200 a year. That same woman could get a 30-yr, $500K TL insurance policy for about $480 a year. If she invested the difference ($3720) every year during that 30 year term, her nest egg would be worth over $700K when it expired (based on 30 years at 10% growth...yes, there are funds that avg 10% since inception). To take it a little further, she could stop investing at that point and let her nest egg grow over the next 15 years until she passes away at the age of 85. At that point a WL policy would pay her beneficiary $500k. (Feel free to prove me wrong, but I have yet to come across a WL policy that pays the beneficiary the Death Benefit AND the accumulated savings over that person's life.) Where as route 2 pays her beneficiary $3 million (For those not following...that $700K will continue to grow at 10% for the next 15 years, ultimately being worth over $3M).

1,000th post!!

That's a good differentiation of the products. Of course, there's really no "right answer" here -- the products are designed for differing degrees of risk tolerance. It just depends on what you're looking for.

BleedBlueGold

Well-known member

- Messages

- 6,300

- Reaction score

- 2,515

That's a good differentiation of the products. Of course, there's really no "right answer" here -- the products are designed for differing degrees of risk tolerance. It just depends on what you're looking for.

Fair enough. I'll leave it at that because I really didn't want to start a debate. I mentioned earlier there are pros/cons to both. I just happen to be partial to term life.

RallySonsOfND

All-Snub Team Snubbed

- Messages

- 2,106

- Reaction score

- 91

1) There shouldn't be any risk once your term expires if you've invested the difference. Your nest egg will be there to take care of you. You won't need a WL policy at that point.

2) Investing the difference in savings from a TL vs WL into a good growth mutual fund would far exceed any cash value developed over the course of your WL policy.

Example: A 40 yr old woman could get a $500K WL insurance policy for about $4200 a year. That same woman could get a 30-yr, $500K TL insurance policy for about $480 a year. If she invested the difference ($3720) every year during that 30 year term, her nest egg would be worth over $700K when it expired (based on 30 years at 10% growth...yes, there are funds that avg 10% since inception). To take it a little further, she could stop investing at that point and let her nest egg grow over the next 15 years until she passes away at the age of 85. At that point a WL policy would pay her beneficiary $500k. (Feel free to prove me wrong, but I have yet to come across a WL policy that pays the beneficiary the Death Benefit AND the accumulated savings over that person's life.) Where as route 2 pays her beneficiary $3 million (For those not following...that $700K will continue to grow at 10% for the next 15 years, ultimately being worth over $3M).

1,000th post!!

You are assuming at the end that she isn't then living off her nest egg too.

irishpat183

Banned

- Messages

- 5,625

- Reaction score

- 504

And you guys against WL (maybe not "against" but critics) are missing the point....It's tax deferred (worth it just for that fact) and you can create your own tax-free income on the back end by taking out loans against the death benny.

And to be honest....most people aren't too excited about mutual funds that don't return anything or that fact that the nest egg may not be there depending on how the market performs.

It's a nice thing to have in your portfolio along with managed money. Life, Annuities, stock....it's good to be diverse.

And to be honest....most people aren't too excited about mutual funds that don't return anything or that fact that the nest egg may not be there depending on how the market performs.

It's a nice thing to have in your portfolio along with managed money. Life, Annuities, stock....it's good to be diverse.

irishpat183

Banned

- Messages

- 5,625

- Reaction score

- 504

1) There shouldn't be any risk once your term expires if you've invested the difference. Your nest egg will be there to take care of you. You won't need a WL policy at that point.

2) Investing the difference in savings from a TL vs WL into a good growth mutual fund would far exceed any cash value developed over the course of your WL policy.

Example: A 40 yr old woman could get a $500K WL insurance policy for about $4200 a year. That same woman could get a 30-yr, $500K TL insurance policy for about $480 a year. If she invested the difference ($3720) every year during that 30 year term, her nest egg would be worth over $700K when it expired (based on 30 years at 10% growth...yes, there are funds that avg 10% since inception). To take it a little further, she could stop investing at that point and let her nest egg grow over the next 15 years until she passes away at the age of 85. At that point a WL policy would pay her beneficiary $500k. (Feel free to prove me wrong, but I have yet to come across a WL policy that pays the beneficiary the Death Benefit AND the accumulated savings over that person's life.) Where as route 2 pays her beneficiary $3 million (For those not following...that $700K will continue to grow at 10% for the next 15 years, ultimately being worth over $3M).

1,000th post!!

You assume that her "investing" would work in her favor..that is the problem.

And WL has liquidity and income options. So it's not like that money is untouchable.

BleedBlueGold

Well-known member

- Messages

- 6,300

- Reaction score

- 2,515

You assume that her "investing" would work in her favor..that is the problem.

And WL has liquidity and income options. So it's not like that money is untouchable.

If her investing isn't working in her favor then she needs a new adviser. While avg 10% yearly short term is pretty unrealistic, this example covers a 45 year span. That sort of long term growth is achievable with the right portfolio.

I'll need a further explanation of your second point to fully understand what you mean. I'm not an expert by any means, but what special liquidity does WL have that any other asset doesn't? What types of income options are you referring to?

Ndaccountant

Old Hoss

- Messages

- 8,381

- Reaction score

- 5,789

You assume that her "investing" would work in her favor..that is the problem.

And WL has liquidity and income options. So it's not like that money is untouchable.

Conversley, you assume that they can't invest the excees money each year in really safe vehicles, like CD's. T-bills, or even funds like VFIIX (which had one year that lost money, less than 1% that year, since inception in 1980 and has a 10 year average return of about 5%).

So really, the idea usually boils down to this. Do you believe that excess growth you can get on your own (risk adjusted) is greater than the return you get on the WL. For some people, they say put it away and forget about it and prefer the WL. Other like to maxamize their savings potential and choose VL. In the end, it's personal choice. But I encourage everyone to really try to understand what you are paying for in insurance, mutual funds, advisors, etc, because you will often be surprised at what you find.